Last April, as the pandemic ravaged New York and unemployment nationwide topped 20%, a global cabal of asset managers sent a cordial letter to drugmakers asking them to “share any relevant findings…drop any enforcement of relevant patents” and generally “put aside any qualms about collaborating with rivals.” Promoting collaboration was a common-sense idea supported by the WHO among others. But what makes this letter interesting is that it was spearheaded by some of the largest shareholders in the respective drug companies, such as index-fund behemoth BlackRock.

This is not how shareholding is supposed to work. If you own a plurality of Pfizer, you want it to do well and make profit at the expense of its competitors, because that’s how you do well. But, as George Mason University economist Alex Tabarrok lays out, the calculus changes if you are an index fund that owns every big company in every industry: if Johnson and Johnson develops a vaccine, Vanguard makes money from its 9% stake. But Vanguard (like the other “institutional investors”) makes even more money if the vaccine is distributed a week earlier, allowing the airlines, restaurant chains and cruise lines in its portfolio to resume normal operations. Tabarrok points out that when Moderna announced promising vaccine news last May, Moderna’s valuation rose by $5 billion, but Boeing’s valuation increased by $8.73 billion.

The big picture view taken by passive investors alarms some economists and antitrust scholars, kindling a growing debate in recent years over whether your pension fund is an oligopolist. Economic theory suggests that “common ownership”—whereby one investor holds major stakes in multiple companies within the same industry—would disincentive the jointly-held companies from competing with each other and potentially lead to less innovation. A somewhat seminal piece of empirical evidence came in 2018, when a study comparing competition on different airline routes found that ticket prices were 3 to 7% higher as a result of funds owning multiple airlines. Similar findings have been published on the banking and pharmaceutical industries. Another study found that firms more heavily owned by index funds had a weaker relationship between CEO pay and competitive performance.

The literature is still developing, and no consensus has been reached on how (or even if) Vanguard and Co. influence the decisions made by companies in their portfolios. But even if index funds create dubious incentives, perhaps they shouldn’t be removed from corporate governance. Some like former Vanguard CEO William McNabb have argued that passive funds are actually better positioned to help firms strategize than other investors since funds are committed to holding indexed companies over the long haul.

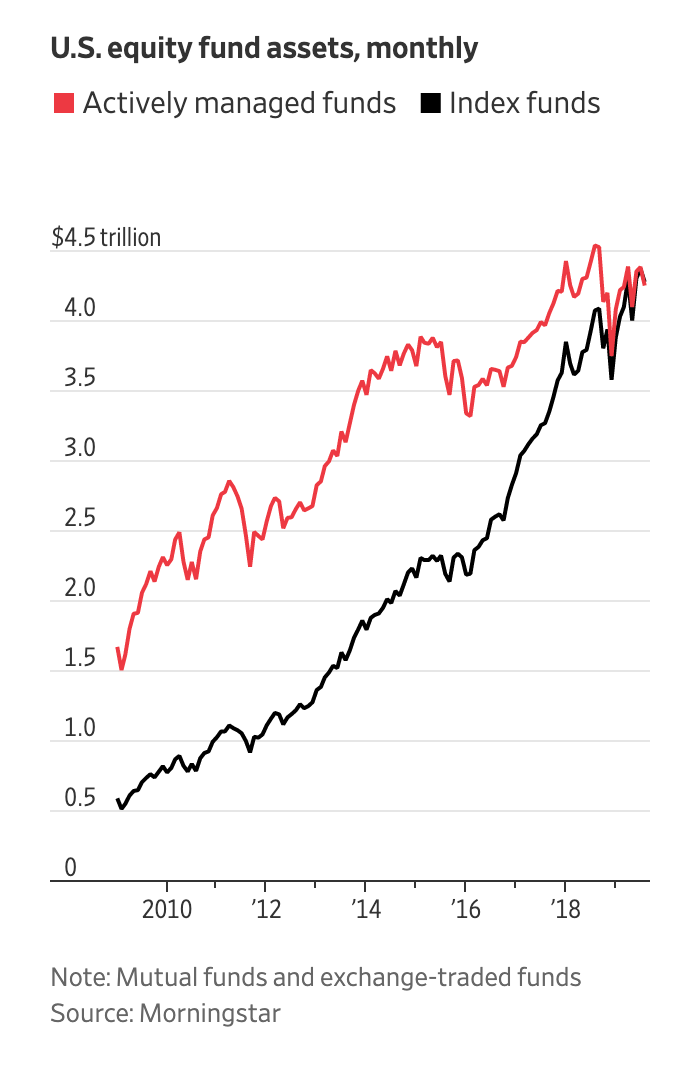

For better or worse, diversified investing is here to stay; index funds now manage more money than their active counterparts. Index funds are boon for the average saver, offering much higher returns (through lower fees magnified by compound interest) and less risk (through diversification). But the antitrust and corporate governance concerns will only grow as index funds (and other passive strategies) become more popular. One paper focusing on the three biggest asset managers—BlackRock, Vanguard and State Street—found that the three firms, taken as one entity, would represent the largest shareholder at 40% of public companies accounting for 80% of total market capitalization.

Even John Bogle—the inventor of the index fund—is worried that index funds might get too big for their britches, writing in the Wall Street Journal that he “ do[es] not believe that such concentration would serve the national interest.” Harvard Law School’s John Coates draws on some Gilded-Age imagery for this situation, dubbing it “The Problem of Twelve”—twelve men from mutual funds sitting around a conference table wielding the keys to American industry.

The academic debate about common ownership centers around what happens when BlackRock owns shares of many companies in a particular market. But Coates hints at a phenomenon even grander in scope and funkier in logic. If the “Big Three” own large parts of most companies, its primary concern is to promote sustainable growth in the economy as a whole—across sectors and in the long run. In pursuing this goal, I feel uneasily like the “Big Three” may erect a kind of quasi-government, with leaders we voted for by depositing our 401ks. Coordinating drug companies to accelerate vaccine research seems like a job for the government—indeed that was the goal of Operation Warp Speed, which did a fine job in this case.

Giving Blackrock CEO Larry Fink and Vanguard CEO Mortimer Buckley significant influence over most major companies is obviously suboptimal, especially given that I can’t think of an effective channel (beyond “public pressure”) to hold these CEOs accountable. However, if BlackRock’s overriding incentive, given it owns all the companies, is to see the economy as a whole do well…I don’t know, a part of me wants to let them try.

One recurring problem in the economy is a failure by individual companies to account for “externalities” of their actions—the costs that e.g. polluters impose on every other creature by damaging the environment. Traditionally—and ideally—fixing externality problems is a task for our elected leaders, held accountable by a mix of elections and activism. But the government hasn’t been known for doing its job these last few years, especially on big picture coordination problems like climate change. So I’m desperate enough to give Wall Street a crack at the issue. If Congress can’t get climate legislation up for a vote in the U.S. Senate, maybe Larry Fink can get it on the agenda of America’s boardrooms (cutting ties with Aramco might be a good start if you’re going to make addressing climate change a centerpiece of your company.)